Interactive Calculator · 2026

TDS on Property — Section 194-IA

The 1% TDS the buyer must deduct and deposit when buying property valued ₹50.00 L or more. Joint-buyer splits, 20% no-PAN rate, NRI-seller flag for Section 195 cases.

Transaction

₹75.00 L

Each buyer files their own Form 26QB for their share.

Seller status

TDS under Section 194-IA

Sale consideration split

On a sale of ₹75.00 L, the buyer withholds ₹0 and pays the seller ₹0 net.

The withheld 1% is deposited with the government via Form 26QB, not paid to the seller in cash. The seller claims credit for it in their ITR.

Sale consideration

₹75.00 L

TDS (1 buyer)

₹75,000

Seller receives (net)

₹74.25 L

Sale − TDS

Rate applied

1%

s.194-IA

Where this ₹0 goes

Buyer deducts

1% at payment

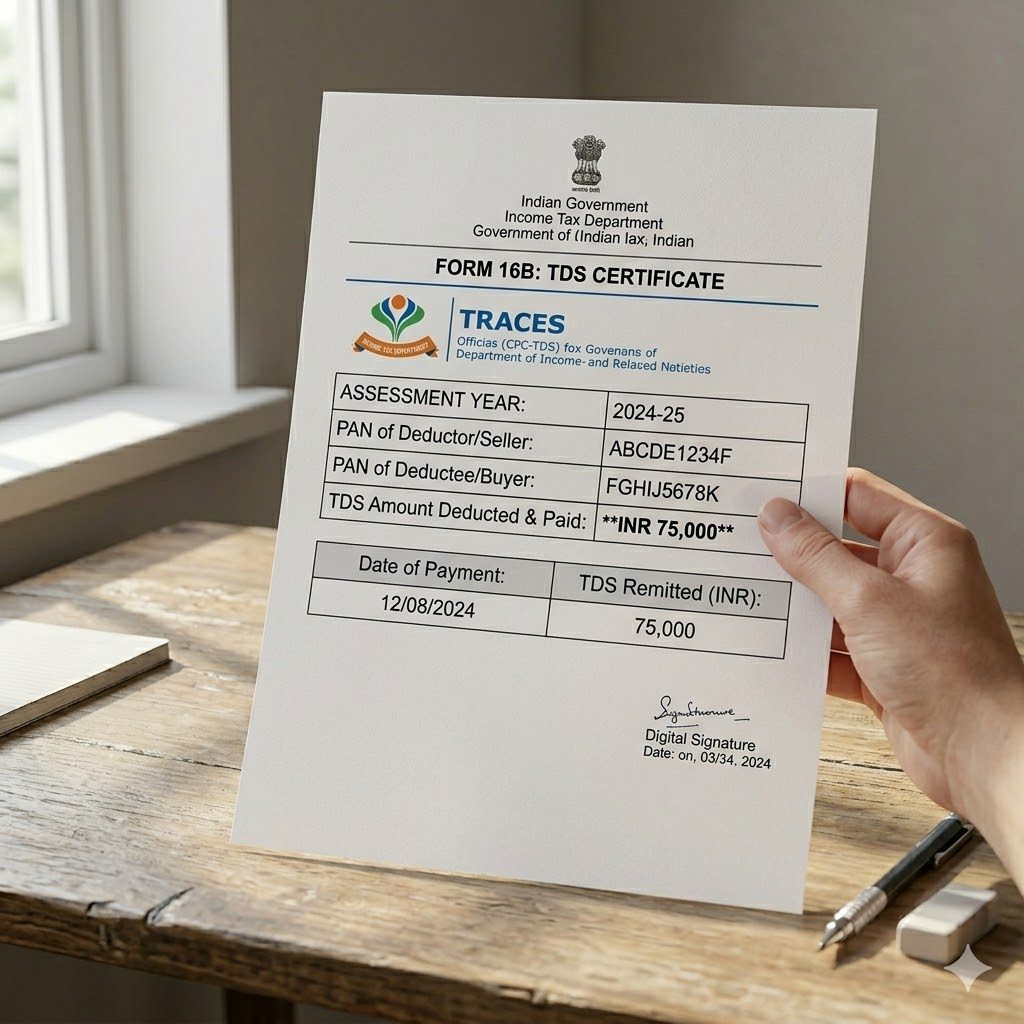

Form 26QB

≤ 30 days, end of mo.

Govt. deposit

TIN-NSDL portal

Form 16B → seller

≤ 15 days from TRACES

TDS on property — process artefacts

Form 26QB

Form 16B

TIN-NSDL portal

TRACES download

Closing the buy — now plan interiors

Once TDS is deposited and registration is done, DesignAI gets your new home ready.

Compliance timeline

- 1Deduct at time of payment. For instalment payments, deduct at every instalment; TDS is on the instalment amount.

- 2Form 26QB (deposit + return) — within 0 days from the end of the month in which deduction was made. File at tin-nsdl.com.

- 3Form 16B (TDS certificate to seller) — within 0 days after Form 26QB is filed. Download from TRACES and hand over to the seller.

Late filing of Form 26QB attracts interest at 1% per month and a late fee of ₹200/day (capped at the TDS amount). Not worth the miss.

How this works

- Threshold ₹50.00 L. Section 194-IA applies only when the total sale consideration is ₹50.00 L or more. The threshold is on the transaction, not on each buyer’s share — so a ₹60 L property bought equally by two co-owners still attracts TDS.

- Buyer is the deductor. You, the buyer, must withhold 1% of the sale price and deposit it with the government. The seller receives 99% of the sale price.

- No-PAN seller → 20%. If the seller has not given you a valid PAN, Section 206AA forces TDS at 20% — a massive jump. Always get the PAN in writing before signing.

- NRI sellers are different. Section 194-IA is silent on non-resident sellers; Section 195 applies, with TDS based on LTCG/STCG at 12.5%/slab rates plus surcharge and cess. Consult a CA — don’t self-serve.

- Agricultural land exempt. Sale of rural agricultural land is outside 194-IA regardless of value.

Deep-dive: TDS on Property Purchase in India — 2026 Guide

Related tools: Stamp Duty Calculator · Capital Gains Tax Calculator · Home Loan Affordability

Indicative only. Always consult a Chartered Accountant for TDS compliance on large transactions. Form 26QB requires both parties’ PAN, property details, date of agreement, date of payment, and sale consideration.

Related Guides — Deep-dive reading

TDS on Property Purchase in India — 2026 Guide

Section 194-IA, the 1% TDS Every Buyer Must Deduct, Form 26QB & Form 16B

ConstructionPremium Apartment Interiors — The ₹15-40 Lakh Tier for Indian 3 BHKs (2026)

Above budget-luxury · Below super-luxury · Materials, brands, contractor-tier reality

Design StylesStamp Duty in India 2026 — State-wise Guide

Rates, Registration Charges, Concessions & How to Calculate Your Liability

ConstructionRelated Tools — You may also find these useful

Acoustic Curtain Calculator

Estimate how much noise and echo heavy, full curtains will dampen — and where they help vs where they can't.

Acoustic ToolAcoustic Door STC Calculator

Work out the STC rating and door build — single leaf, drop seal or sound-lock — to hit your target noise level.

STC CalculatorAcoustic Window Calculator

Estimate how much outside noise a window blocks and the resulting indoor dB level and comfort.

Window Tool