Capital Gains Tax on Property in India — 2026 Guide

LTCG, STCG, Indexation, Section 54, 54EC, 54F & the Budget 2024 Shift

When you sell a flat in Bengaluru you bought a decade ago for ₹40 lakh, for ₹1.5 crore, your bank statement shows a clean ₹1.1 crore profit. Your income tax liability, however, depends on a calculation almost no one outside the CA community gets right on the first try.

Is it long-term or short-term? How much does the Cost Inflation Index reduce the taxable gain? After the Budget 2024 changes, do you pay 12.5% or 20%? Can you shelter part of it in Section 54EC bonds? Will Section 54 exemption fully absorb the gain if you buy another house?

Get any of these wrong and you either overpay Lakhs of rupees in tax, or face a demand notice with interest and penalty two years later when the Assessing Officer catches the omission.

This guide provides the complete 2026 reference — legal framework, indexation math, Finance Act 2024 grandfathering, all three major exemption sections, surcharge rules, and worked examples using real Indian property scenarios.

>

Runs the full calculation for you — holding period, dual-method LTCG comparison, s.54/54EC/54F exemption handling, surcharge, and cess. Useful to have open in a second tab while reading.

The Legal Framework — Two Sentences and a Date

The law that taxes your property gain fits in a paragraph:

- Section 45(1) of the Income Tax Act 1961 charges any profit or gain arising from the transfer of a capital asset to tax under the head "Capital Gains" (Government of India, 1961).

- Section 48 tells you how to compute it: deduct the cost of acquisition and the cost of improvement — indexed for long-term assets — from the full value of consideration received, less any expenditure incurred on transfer.

- The date that changed everything in recent memory: 23 July 2024 — Union Budget day — which replaced the 20%-with-indexation regime with a flat 12.5%-without-indexation rate, subject to grandfathering for immovable property held by resident individuals and HUFs.

Everything else is nuance. Large, expensive nuance.

"Capital gains tax is perhaps the most feared and least understood head under the Income Tax Act. The fear is mostly from the quantum — a single property sale can produce more taxable income than a decade of salary. The misunderstanding is mostly from the sections — there are five major exemptions, each with its own timer, cap, and tripwire." — Dr. Vinod K. Singhania, Direct Taxes Law and Practice (2024, p. 814).

Long-Term vs Short-Term — The 24-Month Rule

The first question in any capital gains calculation: how long did you hold it?

For immovable property (residential flats, villas, land, commercial premises), Section 2(42A) classifies the asset as long-term if held for more than 24 months. Anything 24 months or less is short-term. This 24-month threshold applied from 1 April 2017; before that, the threshold was 36 months (Government of India, 1961, s. 2(42A)).

| Asset class | Long-term threshold |

|---|---|

| Immovable property | > 24 months |

| Listed equity shares, equity mutual funds (s. 111A / 112A) | > 12 months |

| Unlisted shares | > 24 months |

| Gold, debt funds, other assets | > 24 months (from Finance Act 2023) |

Why the Classification Matters

| If STCG (held ≤ 24 months) | If LTCG (held > 24 months) |

|---|---|

| Added to total income | Taxed separately under Section 112 |

| Slab rates (up to 30% + surcharge + cess) | Flat 12.5% (or 20% with indexation — see below) |

| No indexation benefit | Indexation benefit (legacy path only) |

| No Section 54 / 54EC / 54F exemptions | All three exemptions available |

| STCL offsets any capital gain | LTCL offsets only LTCG |

The difference is often enormous. A 2-year holding period makes the same gain 2–4× cheaper to tax.

Day-Precision Trap

The 24 months must be complete calendar months. A property purchased on 15 April 2023 and sold on 14 April 2025 has been held for 23 months and 29 days — one day short — and attracts STCG. Our calculator handles this day-precision correctly; many free online tools round up and silently mislead the user.

The Cost Inflation Index — Indexation, Explained

Cost Inflation Index (CII) is how the government acknowledges that ₹10 lakh in 2010 was worth more than ₹10 lakh in 2024. Without this adjustment, you would pay tax on inflation itself — not on real economic gain.

The CII is notified by the Central Board of Direct Taxes (CBDT) every year, typically around August, via Notification under Section 48 Second Proviso. The base year is FY 2001-02 = 100 (rebased from the earlier 1981-82 base, effective AY 2018-19, via Finance Act 2017).

How Indexation Works

The indexed cost is computed as:

Indexed Cost of Acquisition = Purchase Price × (CII of Sale Year ÷ CII of Purchase Year)

CII Table — Every FY Since Rebase

| Financial Year | CII | Financial Year | CII |

|---|---|---|---|

| 2001-02 (base) | 100 | 2013-14 | 220 |

| 2002-03 | 105 | 2014-15 | 240 |

| 2003-04 | 109 | 2015-16 | 254 |

| 2004-05 | 113 | 2016-17 | 264 |

| 2005-06 | 117 | 2017-18 | 272 |

| 2006-07 | 122 | 2018-19 | 280 |

| 2007-08 | 129 | 2019-20 | 289 |

| 2008-09 | 137 | 2020-21 | 301 |

| 2009-10 | 148 | 2021-22 | 317 |

| 2010-11 | 167 | 2022-23 | 331 |

| 2011-12 | 184 | 2023-24 | 348 |

| 2012-13 | 200 | 2024-25 | 363 |

Worked Example — Indexation Saves Lakhs

Assume you bought a 3BHK in Pune on 1 June 2012 for ₹60 lakh. Sold on 1 June 2024 for ₹1.8 crore, no improvements, ₹2 lakh brokerage. Holding period: 12 years, clearly LTCG.

| Line item | Value |

|---|---|

| Purchase price | ₹60,00,000 |

| Purchase FY | 2012-13 (CII = 200) |

| Sale FY | 2024-25 (CII = 363) |

| Indexed cost | 60,00,000 × (363 ÷ 200) = ₹1,08,90,000 |

| Sale price | ₹1,80,00,000 |

| Transfer expenses | ₹2,00,000 |

| Net sale consideration | ₹1,78,00,000 |

| Indexed LTCG | 1,78,00,000 − 1,08,90,000 = ₹69,10,000 |

| Unindexed LTCG | 1,78,00,000 − 60,00,000 = ₹1,18,00,000 |

Without indexation the "gain" is ₹1.18 crore. With indexation it's ₹69 lakh. On the sale being pre-Budget-2024-cutoff, the taxpayer picks whichever rate-and-base combination produces lower tax:

- 12.5% × 1,18,00,000 = ₹14,75,000 base tax

- 20% × 69,10,000 = ₹13,82,000 base tax

The second method wins by ₹93,000 on the base before cess and surcharge. Multiply across millions of property transactions and the Finance Act 2024's grandfathering clause represents real savings for pre-cutoff holders.

The Budget 2024 Shift — What Changed on 23 July 2024

Finance Minister Nirmala Sitharaman's 2024 budget speech introduced the single biggest capital-gains reform in over two decades (Ministry of Finance, 2024). For real estate specifically:

1. Abolished indexation for sales on or after 23 July 2024.

2. Reduced the rate from 20% to 12.5% on long-term capital gains.

3. Grandfathered pre-cutoff holders: for immovable property acquired before 23 July 2024 by resident individuals and HUFs, the taxpayer may compute the tax using either the new 12.5% without indexation or the old 20% with indexation — whichever is lower.

Who Gets the Election?

| Taxpayer type | Asset bought before 23 Jul 2024 | Asset bought on/after 23 Jul 2024 |

|---|---|---|

| Resident individual / HUF | Choose lower of 12.5% (no indexation) or 20% (indexed) | Flat 12.5% no indexation |

| Non-resident (NRI) | Flat 12.5% no indexation (indexation benefit withdrawn) | Flat 12.5% no indexation |

| Company, firm, LLP | Flat 12.5% no indexation | Flat 12.5% no indexation |

The grandfathering clause was the government's concession to a political pushback from middle-class homeowners who had bought long-held properties counting on the indexation benefit. It applies only to individuals and HUFs who are residents and only to immovable property — not to gold, debt funds, or any other asset class.

"The restoration of choice for pre-cutoff property was a rare instance of a budget proposal being softened within three weeks of presentation. It reflects the Finance Ministry's recognition that a retroactive removal of a legitimately earned tax benefit creates genuine hardship, not just notional tax." — T. N. Ninan, India's Turn: Tax and Policy (2025, p. 141).

Practical Guidance

- Sold before 23 Jul 2024: old regime only — 20% with indexation.

- Sold on/after 23 Jul 2024, bought before: election available. Our calculator computes both methods and highlights the lower.

- Sold on/after 23 Jul 2024, bought on/after: 12.5% without indexation, no choice.

Section 54 — The Primary Exemption

The single most valuable exemption for homeowners selling one residence and buying another. Under Section 54 of the Income Tax Act, 1961:

1. The asset sold must be a long-term residential house (land or building).

2. The taxpayer must invest the capital gain in another residential house in India.

3. Timeline: purchase within 1 year before or 2 years after the sale date, or construct within 3 years of the sale.

4. The new property must be held for at least 3 years — sell sooner and the exemption is clawed back.

5. Cap introduced by Finance Act 2023: exemption capped at ₹10 crore (applicable from AY 2024-25).

Capital Gain Accounts Scheme (CGAS)

If you cannot invest the full amount before your income tax return filing deadline (typically 31 July of the following year), deposit the unutilised amount in a Capital Gain Accounts Scheme account with a public sector bank. You then have until the full 2 or 3-year deadline to actually invest. Failure to do so within the period causes the unutilised amount to become taxable in that later year.

| CGAS type | Use case |

|---|---|

| Type A (savings) | Short-term parking, can be withdrawn anytime for purpose |

| Type B (term deposit) | Higher interest, fixed term aligned with s.54 deadline |

Worked Example — Full Section 54 Shelter

You sell your Mumbai 2BHK in July 2025 at an LTCG of ₹80 lakh (after indexation). You identify and sign the agreement for a ₹1.2 crore replacement flat in Pune by December 2025. You take possession in March 2026.

| Line item | Value |

|---|---|

| Indexed LTCG | ₹80,00,000 |

| Reinvestment in new residential property | ₹1,20,00,000 |

| Exempt under s.54 | ₹80,00,000 (fully absorbed) |

| Taxable LTCG | ₹0 |

| Tax payable | ₹0 |

Your entire gain is sheltered. This remains one of the most powerful deferrals in the Indian tax code.

The Single-House Rule (FY24)

Finance Act 2023 introduced a crucial constraint. Prior to AY 2024-25, Section 54 allowed exemption for investment in two residential houses in a lifetime (subject to LTCG not exceeding ₹2 crore). From AY 2024-25, exemption is allowed only for one residential house, period. The two-house option is gone.

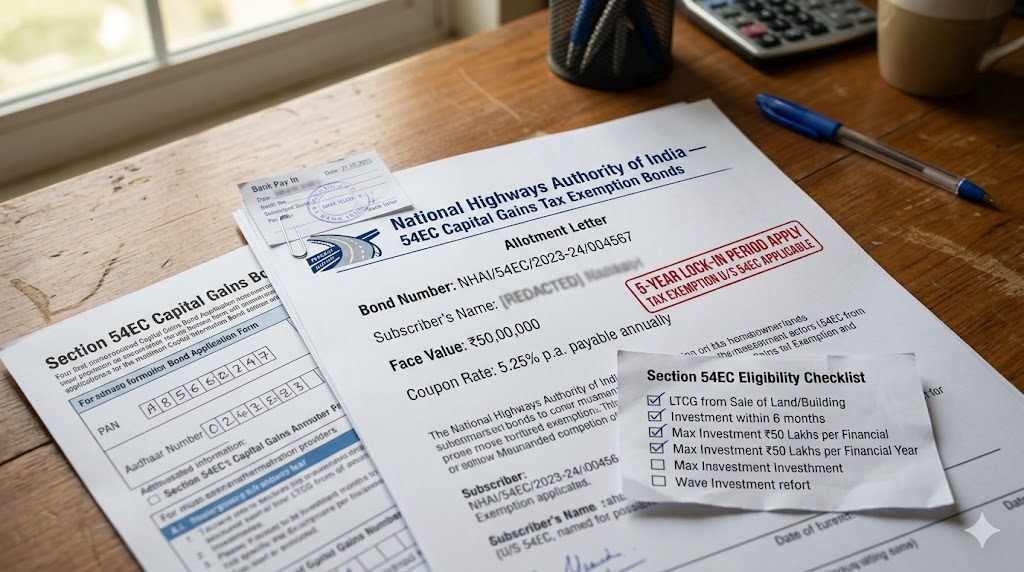

Section 54EC — Capital Gain Bonds

If you don't want to reinvest in another property, Section 54EC lets you defer tax by investing in a specific list of government-backed bonds:

- NHAI (National Highways Authority of India)

- REC (Rural Electrification Corporation)

- PFC (Power Finance Corporation)

- IRFC (Indian Railway Finance Corporation)

Terms

| Parameter | Rule |

|---|---|

| Investment window | 6 months from date of transfer |

| Aggregate cap | ₹50 lakh per taxpayer per financial year (Finance Act 2018) |

| Lock-in | 5 years (up from 3 years, also Finance Act 2018) |

| Current coupon | Approximately 5.25% p.a. (FY 2025-26 tranches) |

The ₹50 lakh cap is shared across all Section 54EC investments in a year. You cannot split ₹50 lakh into NHAI and another ₹50 lakh into REC — the total caps at ₹50 lakh.

When 54EC Makes Sense

1. Smaller gains. For a gain under ₹50 lakh, 54EC can fully shelter it with minimal commitment (bonds, not a house).

2. No replacement property plans. If you're selling to rebalance into equity, 54EC is a 5-year waiting room.

3. Partial shelter. Use 54EC for ₹50 lakh + Section 54 for the rest on the same transaction.

Worked Example — Combined s.54 + s.54EC

You sell a Delhi villa in August 2025 with an indexed LTCG of ₹2 crore. You buy a smaller Gurgaon flat for ₹1.4 crore by January 2026 (Section 54) and subscribe to ₹50 lakh of REC 54EC bonds by February 2026.

| Line item | Value |

|---|---|

| Indexed LTCG | ₹2,00,00,000 |

| Section 54 exemption (Gurgaon flat cost) | ₹1,40,00,000 |

| Section 54EC exemption (REC bonds cap) | ₹50,00,000 |

| Taxable LTCG | ₹10,00,000 |

| Tax @ 20% (with surcharge + cess if applicable) | ~₹2,08,000 |

The combination drops your tax from ~₹41 lakh (unexempted) to ~₹2 lakh — a 95% reduction entirely within the letter of the law.

Section 54F — The Non-House Variant

Section 54F is the parallel to Section 54 for any long-term capital asset other than a residential house — gold, debt funds, unlisted shares, land (without building). If you sell such an asset and reinvest in a residential house, s.54F lets you shelter the gain, subject to:

1. Single-house ownership rule: you must not own more than one other residential house at the time of transfer.

2. Proportional deduction: if you reinvest only part of the sale consideration (not just the gain), exemption is prorated:

Exempt LTCG = LTCG × (Amount Invested ÷ Net Sale Consideration)

3. Same timelines as Section 54 (1 year before / 2 years after / 3 years construction).

4. Same ₹10 crore cap post Finance Act 2023.

This is less commonly used for pure property sales (Section 54 applies directly), but is important when you're selling land (without a building) and buying a house — s.54F is the right section.

Surcharge & Cess — The Stacking Rules

Base tax is only part of the story. Two multipliers follow.

Surcharge

A percentage of the base tax, triggered by total income level:

| Total income | General surcharge | Surcharge on capital gains (s.112 / 112A) |

|---|---|---|

| ≤ ₹50 L | 0% | 0% |

| ₹50 L – ₹1 Cr | 10% | 10% |

| ₹1 Cr – ₹2 Cr | 15% | 15% |

| ₹2 Cr – ₹5 Cr | 25% | 15% (capped) |

| > ₹5 Cr | 37% (new regime: 25%) | 15% (capped) |

The 15% cap on capital-gains surcharge was introduced by Finance Act 2022 (effective FY 2022-23 onwards). Before that, ultra-high-income taxpayers could face a 37% surcharge on LTCG — which created powerful incentives to route property sales through companies or trusts. The cap eliminated that arbitrage.

Health & Education Cess

A flat 4% on (tax + surcharge). Applies to everyone, no exemptions.

Worked Example — Full Tax Stack

Continuing the Pune example from earlier: indexed LTCG of ₹69.10 lakh, taxpayer's total income ₹75 lakh (falls in the 10% surcharge bracket):

| Step | Calculation | Amount |

|---|---|---|

| Base tax @ 20% | 69,10,000 × 20% | ₹13,82,000 |

| Surcharge @ 10% | 13,82,000 × 10% | ₹1,38,200 |

| Sub-total | ₹15,20,200 | |

| Health & Education Cess @ 4% | 15,20,200 × 4% | ₹60,808 |

| Total tax | ₹15,81,008 |

Effective rate on the indexed gain: 22.88%.

Common Mistakes That Cost Lakhs

Mistake 1 — Forgetting the 6-Month 54EC Window

Taxpayers often file their returns in July of the following year, by which time the 6-month 54EC window has already closed. The 6 months is from the date of transfer, not the end of the financial year. A May 2025 sale must be bonded by November 2025 — not March 2026.

Mistake 2 — Holding the New Property Under 3 Years

Section 54 claws back the exemption if the replacement property is sold within 3 years. The claw-back is computed by reducing the cost of the new property by the exempted gain. Result: the earlier-sheltered gain becomes taxable in the year of the second sale.

Mistake 3 — Counting Joint Agreement Date Instead of Registration

For Section 54, the critical date is the date of transfer, which is the registration date (stamp duty paid, sub-registrar signed) — not the booking date or agreement-to-sell date. A flat booked in April 2023 but registered in September 2025 starts its holding period from September 2025, not April 2023.

Mistake 4 — Ignoring Stamp Duty Value (Section 50C)

If the declared sale consideration is less than the stamp duty value (circle rate) by more than 10%, Section 50C deems the stamp duty value as the sale consideration for tax purposes — increasing the capital gain. You cannot under-report the sale price to reduce tax.

Mistake 5 — Missing Indexation on Improvement Cost

Structural additions (an extra floor, major renovation with capital character) qualify as cost of improvement and are separately indexed from the year of improvement — not the year of original purchase. Many taxpayers either forget to claim them or index from the wrong year.

Mistake 6 — Confusing Section 54 with 54F

Sale of a house: Section 54 applies (any number of other houses owned).

Sale of land alone / gold / shares: Section 54F applies (limit one other house at time of transfer).

Filing under the wrong section is the single most common capital gains scrutiny trigger.

Pre-2001 Purchases — The FMV Substitution

For immovable property acquired before 1 April 2001, you have the statutory right to substitute the Fair Market Value as of 1 April 2001 for your actual (much lower) purchase price. This is invaluable for ancestral property — land bought in the 1970s for ₹2 lakh might have a 2001 FMV of ₹40 lakh, which then gets indexed forward through the CII.

How to Establish FMV

- Registered valuer report — the gold standard; CA/IT department accepts without question.

- Stamp duty value as on 1-Apr-2001 — available from state registration portals for many properties.

- Comparable sale instances — secondary evidence only.

For our calculator, enter the FMV as of 1 April 2001 (not the original purchase price) in the Purchase Price field when the asset was bought before the base year. The calculator handles the rest.

Capital Losses — Setoff and Carry-Forward

If your sale produces a loss (sale price below indexed cost), it's not wasted — it's a tax shield.

| Loss type | Setoff in same year against | Carry-forward |

|---|---|---|

| STCL (short-term) | Any capital gain (short or long) | 8 assessment years |

| LTCL (long-term) | Only LTCG | 8 assessment years |

You must file your income tax return by the due date to carry the loss forward. A belated return forfeits the carry-forward right, though it preserves the same-year setoff.

Filing — How the ITR Captures Capital Gains

Capital gains are reported in ITR-2 or ITR-3 under Schedule CG (Capital Gains). The schedule has separate sections for:

- Short-term gains (by asset class)

- Long-term gains (by asset class)

- Exemption claims under each Section (54, 54B, 54EC, 54F, 54GA, 54GB)

- Loss carry-forward from prior years

Documents to Keep

1. Sale deed (registered) — proves transfer date and sale value.

2. Purchase deed or allotment letter — proves acquisition date and cost.

3. Payment proofs for acquisition — bank statements, cheques, receipts.

4. Brokerage invoices and stamp duty receipts — for the cost basis.

5. Improvement invoices with dates — for indexed improvement cost.

6. Section 54 proofs — registered agreement of new property, CGAS statements.

7. 54EC bond subscription receipts — from NHAI/REC/PFC/IRFC.

8. Valuation report — if substituting FMV as of 1 April 2001.

Looking Ahead — Expected 2026-27 Changes

Three areas to watch in the next Union Budget:

1. CII rebase. The last base-year change was 2017 (from 1981-82 to 2001-02). The 25-year CII series is now approaching an awkward length; a rebase to 2012-13 or 2017-18 is under internal discussion at the Finance Ministry.

2. Section 54 cap indexation. The ₹10 crore cap is not indexed; with Mumbai and Delhi property appreciation, this will start to bite metro homeowners in the next 3–5 years.

3. 54EC bond cap revision. The ₹50 lakh cap has been static since 2014. Industry associations have requested revision to ₹1 crore, but Treasury resistance has been consistent.

Open the Calculator

>

Enter purchase date, purchase price, sale date, sale price, and any improvements or reinvestments. The calculator auto-detects STCG vs LTCG, handles indexation via the official CII table, runs both 12.5%-without and 20%-with methods for pre-cutoff purchases, applies Section 54 and 54EC caps, and adds surcharge and cess. Updated with the latest CBDT notifications.

Related tools:

- Stamp Duty Calculator — closing costs on property purchase

- EMI Calculator — home loan + tax savings under Section 24

- Cost Calculator — construction + interior costs

References

- Central Board of Direct Taxes (2024) Cost Inflation Index for Financial Year 2024-25: Notification No. 44/2024. New Delhi: Ministry of Finance.

- Central Board of Direct Taxes (2023) Clarifications regarding Section 54/54F cap of ₹10 crore: Circular No. 4/2023. New Delhi: Ministry of Finance.

- Government of India (1961) Income Tax Act, 1961 (as amended by Finance Act 2024). New Delhi: Ministry of Law and Justice.

- Government of India (2023) Finance Act 2023. New Delhi: Ministry of Finance.

- Government of India (2024) Finance (No. 2) Act, 2024. New Delhi: Ministry of Finance.

- Income Tax Department (2024) Income Tax Return Form ITR-2 — Instructions for AY 2024-25. New Delhi: Central Board of Direct Taxes.

- Ministry of Finance (2024) Budget Speech 2024-25. New Delhi: Government of India, 23 July.

- Ninan, T. N. (2025) India's Turn: Tax and Policy. New Delhi: Penguin India.

- Singhania, V. K. (2024) Direct Taxes Law and Practice. 65th edn. New Delhi: Taxmann Publications.

Author's Note: This guide reflects the law as amended by Finance (No. 2) Act 2024 and subsequent CBDT notifications through April 2026. The Cost Inflation Index values are published annually by CBDT under Section 48 Second Proviso — always verify the latest CII before computing. The grandfathering clause applies to resident individuals and HUFs only; non-residents and corporate taxpayers are on the post-cutoff regime regardless of purchase date.

Disclaimer: This article is for informational and educational purposes only. It does not constitute tax, legal, or financial advice. Capital gains computation depends on document-specific facts, acquisition history, prior-year losses, and the taxpayer's full income picture. Consult a qualified Chartered Accountant before filing an ITR with a capital gain entry. The calculator and this guide produce estimates; the final tax liability is determined by the Assessing Officer on the basis of your return and supporting evidence.

Export this guide

Related Guides — Deep-dive reading

Stamp Duty in India 2026 — State-wise Guide

Rates, Registration Charges, Concessions & How to Calculate Your Liability

ConstructionHome Loan Affordability in India — 2026 Guide

FOIR, LTV, EMI, Tax Benefits, Bank Comparisons & How Much House You Can Actually Buy

ConstructionHome Renovation Cost in India — The Homeowner's Working Reference

Five Renovation Scopes, the Renovate-vs-Build-New Decision, Cost Breakdown, Room-by-Room Priorities & Ten Hidden Costs

Cost & MoneyRelated Tools — Try Free

Capital Gains Tax Calculator — Property

LTCG and STCG on property sale with Cost Inflation Index (CII) indexation, Section 54 and 54EC exemptions, and Budget 2024 dual-method comparison.

Capital GainsStamp Duty Calculator — All Indian States

Stamp duty + registration charges for all 28 states and 8 UTs — gender concessions, urban/rural variants, metro cess built in.

Stamp DutyHome Loan EMI Calculator — 2026

Monthly EMI, total interest, tax savings, and year-by-year amortization across 10 bank rates.

EMI Calculator